The Confidential Information Memorandum series

Chapter 1: Introduction and the Executive Summary section

What a Confidential Information Memorandum Really Looks Like

If you’ve ever worked on an M&A process, chances are you’ve spent an unhealthy amount of time inside a Confidential Information Memorandum — or CIM.

For private equity funds, strategics, lenders and advisors, the CIM is the core marketing document of a sell-side process. It is the document that turns a company into an investment story.

Despite the name “memorandum,” modern CIMs are almost always PowerPoint presentations rather than Word documents.

Note: I know there are a few examples on the internet in word format stating that those are example of CIMs but you can really feel the 90’s vibe hitting and I can guarantee you that is not even slightly similar to what you will have to produce working inside an Investment Bank (that is actually the reason why I created this series). Honestly PPTs are the absolute standard, full stop.

Older-style Information Memorandums used to be much more text-heavy, but today the format is highly visual: charts, market data, operational diagrams, financial bridges and graphic concepts representations are the way to go.

And CIMs are long. A standard one is usually somewhere between 100 and 200 pages, depending on the complexity of the business and the competitiveness of the process.

Before the CIM is distributed, buyers are typically shown a shorter document called a Teaser.

The teaser is essentially a stripped-down and partially anonymized extract of the CIM used to test investor interest before disclosing sensitive information. Think of it as the trailer before the full movie.

Once investors sign an NDA, they receive the full Information Memorandum.

Interestingly, despite looking extremely detailed and customized, most CIMs follow almost exactly the same structure.

Usually, the document revolves around six core sections:

Executive Summary

Key Investment Highlights

Market Overview

Company Overview

Growth Strategy

Financial Overview

Everything else is essentially an expansion of these sections through operational deep dives, product analyses, market studies and detailed financial schedules.

And ultimately, the entire document exists to answer just five fundamental investment questions:

Is the market attractive and growing?

Is the company better than competitors?

Does it have a differentiated product?

Is management capable of executing?

Does the business generate strong financial returns?

That’s it.

Every section of the CIM — from the market overview to the operations slides to the growth strategy — is built to support one or more of these points.

Once you understand this, CIMs become much easier to read (or draft if you are on the other side of the table).

And interestingly, you also start realizing that most investment processes are ultimately exercises in structured storytelling.

A good CIM is not simply presenting information, it is building conviction. Which brings me to the real point of this article: walk you through each section of the CIM and its typical slides looking at them through the lenses of their “so what”. Because the first lesson of CIM analysis — and frankly of any financial presentation — is that every single slide needs one clear takeaway. One thing the reader should walk away with immediately, without having to work for it. That is what separates a good and clear presentation from a bad one. A graphic example will be provided as well.

1. Executive Summary

The Executive Summary is usually the most important section of the entire CIM together with the Key Investment Highlights.

Why?

Because this is where investors form their first impression of the asset. Most people in a process will not read the full document immediately. They will first skim the Executive Summary to decide whether the opportunity deserves further attention.

The objective of this section is therefore very simple:

explain the business, the investment case and the attractiveness of the opportunity in the clearest possible way.

Investors immediately want to understand:

what the company actually does;

where revenues come from;

how diversified the business is;

whether the company already looks scalable and institutionalized;

and whether the platform visually “looks like” a quality asset.

Typically, the Executive Summary includes the following slides:

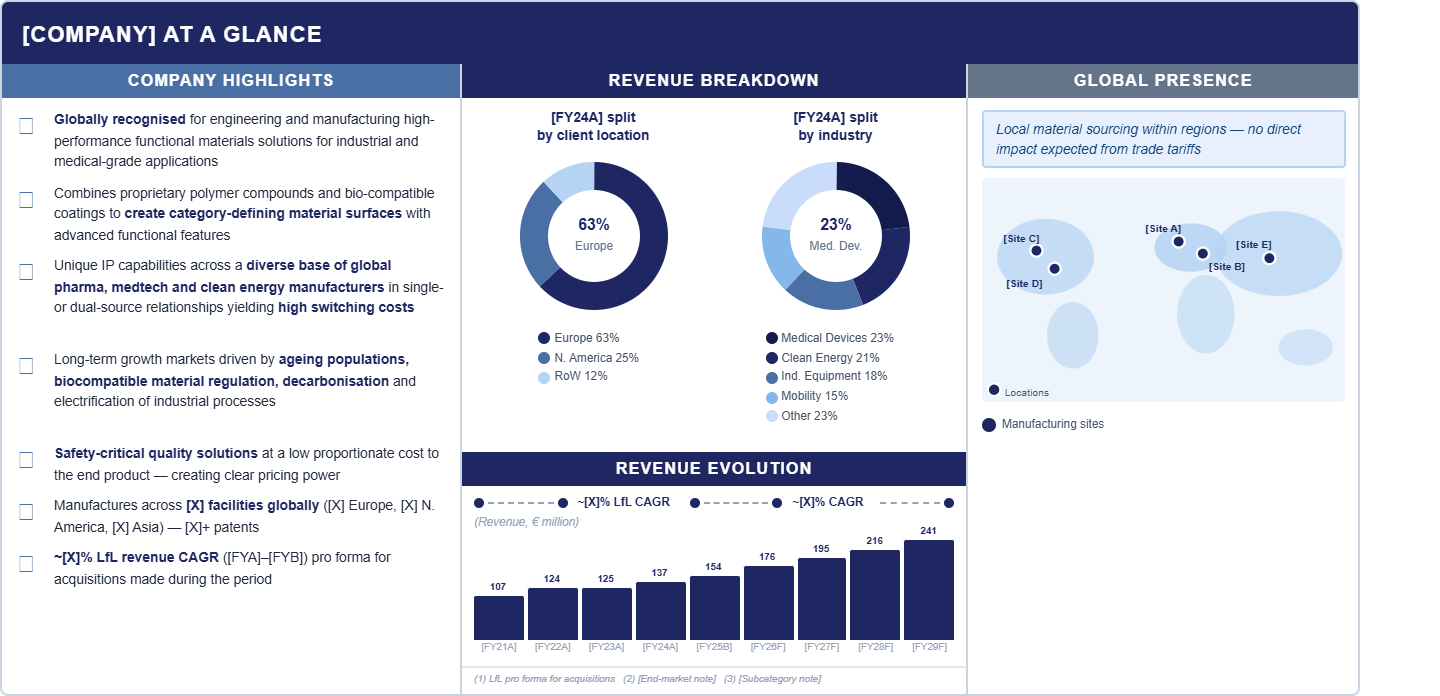

Company at a glance: a short introductory description of the company.

So what: in a single page, an investor should immediately understand what the company does, how it does it, and how those capabilities translated into financial performance.

What you will typically find: company description, unique value proposition, revenue breakdown by geography and product line, key customer and supplier information, facilities footprint, and a snapshot of historical financials — usually including a budget or forecast for the current or following year depending on when the CIM hits the market.

Behind the scenes: this is usually a summary of the summary where all the key messages of the memo are condensed and although it seems rather easy is usually one of the most difficult slide to make because of the need to be extremely clear and concise.

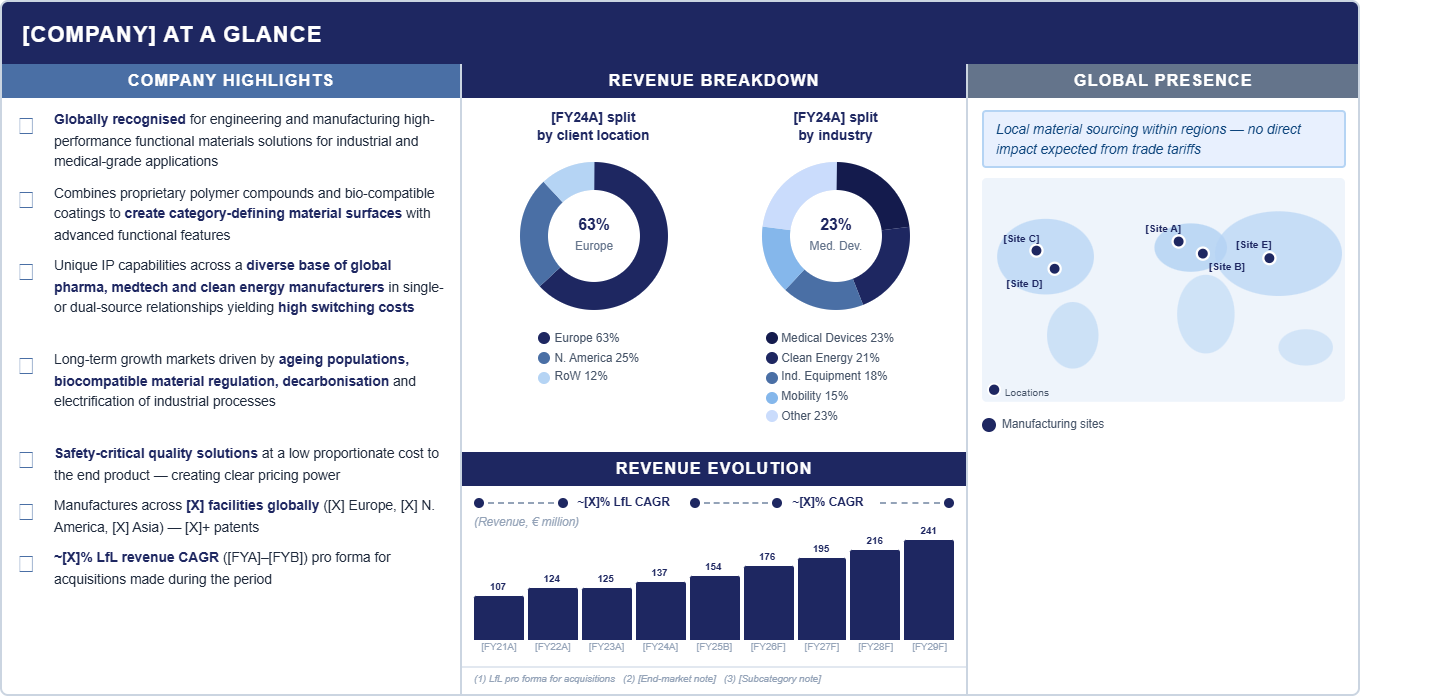

History of the company most times paired with historical financials: overview of the company historical development.

So what: give context on how the company became what it is today and demonstrate how it responded to challenges along the way. A company that has grown consistently through different macro environments is a more compelling investment than one with a clean but shallow track record.

What you will typically find: a timeline of key milestones — founding, acquisitions, product launches, ownership transitions — often backed by a revenue evolution chart to show how those events influenced key financials.

Behind the scenes: an additional question to which this slide most times is quietly answering is: why is this asset for sale right now? The history slide is the first place the bank starts constructing that answer (you don’t want to buy just because the entrepreneur think there is no futher room for growth right? you want to invest in a development project).

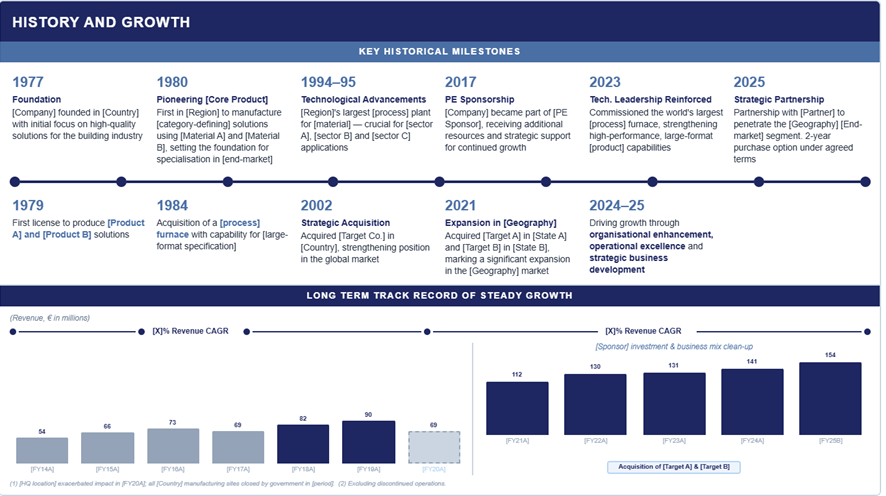

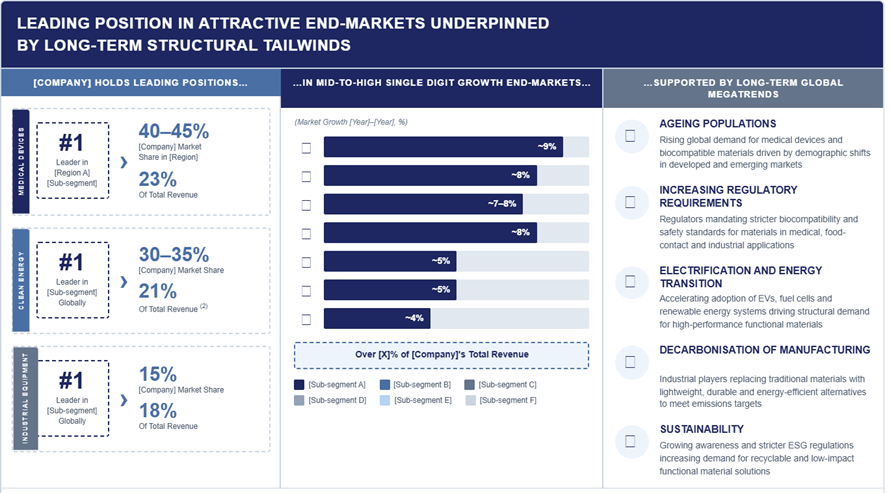

Products/services overview and related end-markets:

So what: show what the company sells and make clear it operates in the most attractive segments of its market — ideally from a position of leadership.

What you will typically find: a portfolio breakdown with revenue share by division, end markets, and addressable market size. In services businesses, headcount by division often appears here too.

Behind the scenes: the revenue split by product line is one of the most scrutinised elements on this slide. A company that describes itself as a diversified platform but generates seventy percent of revenue from a single product is a very different investment from what the narrative suggests. Read the percentages and where value stands before you read the words.

Market overview and growth trends:

So what: justify the growth assumption embedded in the financial projections. The sector is large, it is growing, and the underlying trends are structural rather than cyclical (ideally ofc, if not there need to be some kind of explanation).

What you will typically find: market sizing, projected growth rates, key demand drivers, and competitive landscape positioning.

Behind the scenes: markets in CIMs are always growing (lol) so if you are an investor always cross-check the assumptions against other sources and common sense of where the world is going (niche sub-segment data can paint a more attractive picture than the broader market). If there are Vendor Due Diligences available those information will likely come from there.

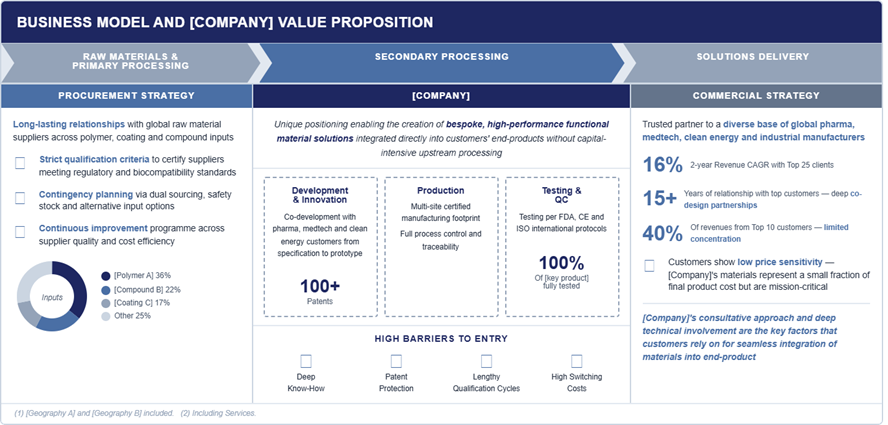

Company business model and unique value proposition: the most misread section of a CIM. Not the same as the product overview, this shows how it the company operates i.e. how it makes money by doing what it does in a distinctive way (hopefully).

So what: represent the full value chain — from suppliers to clients — and demonstrate that the model is structurally difficult to replicate and built on relationships that do not disappear when ownership changes.

What you will typically find: value chain representation, supplier and client breakdown generally trying to highlight low concentration on both sides or explaining high concentration dynamics and a breakdown of the company core value creation processes.

Behind the scenes: “difficult to replicate” has a very specific meaning here. You are looking for concrete moats — long customer qualification cycles, regulatory certifications that take years to obtain, proprietary processes, switching costs high enough that a client would rather absorb a price increase than requalify an alternative supplier. When a CIM says “strong competitive positioning,” your job is to ask: what specifically makes this hard to replicate, and how long would it take a well-funded competitor to try? If you cannot find the answer in this slide, that is itself a signal.

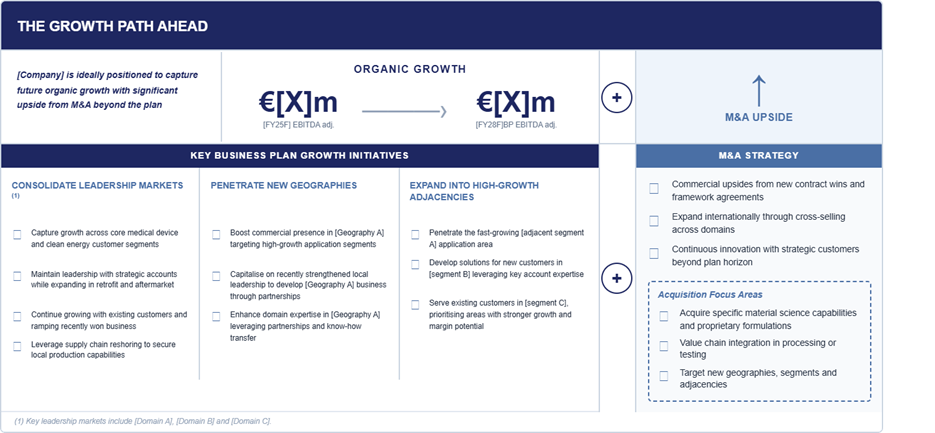

Growth strategy:

So what: show how the company intends to grow and why it is the right player to execute that plan.

What you will typically find: a split between organic growth initiatives — new geographies, new products, pricing, operational improvements — and M&A, usually framed as a consolidation opportunity in a fragmented market.

Behind the scenes: the key question is always the same — how much of the projected growth is already happening, and how much depends on things that have not happened yet? Organic initiatives backed by signed contracts are visibility. Everything else is a bet. On M&A specifically: including an acquisition pipeline in a CIM is not just informative. The bank selling the company is simultaneously positioning itself to advise on the add-ons that will fuel the projected growth post-closing. You are not just reading an investment thesis. You are reading (or preparing) a pitch for future mandates.

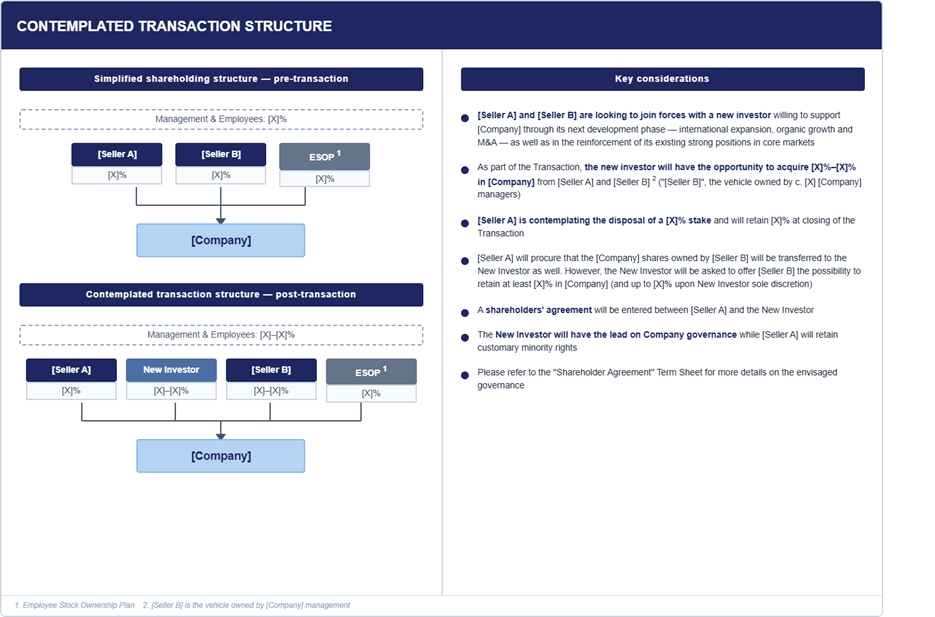

Process overview and envisaged transaction structure:

So what: make the reader understand exactly what is being sold, who is selling it, and how the process will unfold.

What you will typically find: a legal structure chart pre and post transaction, a description of which entities are included in the perimeter, and an overview of the process steps — NDA, management presentation, indicative offer, due diligence, binding offer, signing, closing.

Behind the scenes: this slide is more tactical than else, it allows the seller to “make the first move” and set the tone for what it expects from investors.

As you can see, a well-constructed Executive Summary already builds the first layer of the investment case — what the company does and how it operates. Coupled with the Key Investment Highlights, it gives you the full picture of why you should invest. This is the pyramid principle at work: conclusion first, evidence second. Everything that follows in the CIM — the market deep dive, the operational detail, the financial schedules — exists only to defend and support those two layers under scrutiny, not to build them from scratch.

In the next piece, we move into the Key Investment Highlights — where the bank states explicitly why this is an attractive investment and spends the rest of the document proving it.

Here is the closest example of a real CIM I found:

chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://uploads-ssl.webflow.com/5b8488e07e20b8a104400c72/5bb7f81b231fc90216d01183_cim-ppt-sample-1.pdf

Reminds me the good old times in IB

Reminds me the good old times in IB